Potential COVID-Driven Go-to-Market Adjustments for the Healthcare Industry

Part One: Health Care

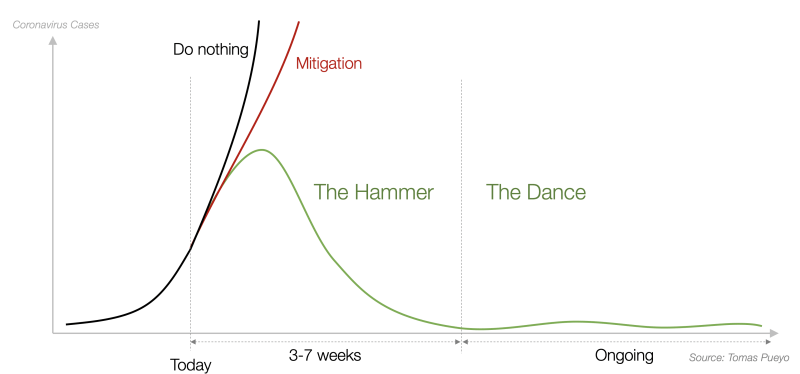

Early on in the pandemic, an influential article—The Hammer and the Dance—was published in The Medium attempting to predict the course of society’s response to COVID-19. Whether you agreed with the data science, it was an interesting thought piece that most definitely affected policy. It argued that the initial response to COVID must be a harsh, months-long lockdown to bring R—the virus reproduction rate—below 1. At that point, restrictions could be gradually lifted, but a dance would ensue whereby flare-ups in infection would result in more targeted restrictions, localized geographically, and through time. By this method, Pueyo argued, society could keep the virus at manageable levels until either a vaccine was mass-distributed or some level of herd immunity had been reached.

This general theory has proven to be a remarkably accurate forecast across the world. While there have been outliers—Sweden and Brazil on the lax side and China on the ultra-strict side—countries have generally gone through a period of radical change, and this has been followed by the beginnings of “the dance”, as small outbreaks are contained, quickly, with rapid data feedback.

As countries and individuals have gone, so have companies. Companies went into months-long retrenchments and reassessments of their businesses starting in early March. Industries had dramatically different responses, but they learned quickly. Agility was forced on millions of companies as they struggled to synthesize huge amounts of ever-changing information that changed daily. As of late June, the “hammer” period is over, and now companies have largely transitioned to the “dance.” The most successful companies will be those that react to data the quickest, with local-level execution.

Covid-19 has shown a harsh spotlight on the annual planning cycle’s deficiencies. How many companies are even referring to the plans that they so proudly put together six months ago? Instead, successful firms are “planning in pencil”, with real-time instrumentation and nimble and empowered teams to make decisions quickly and discretely.

This is the first of three articles on how industries are reacting to the agile mandate in the age of Covid-19, focused on health care, with a particular focus on go-to-market issues. We have already seen health care change more in three months than it has in years—but the hard work remains ahead. It remains to be seen whether providers, payers, and drug companies will use the opportunity created by COVID to permanently change how they operate, but there are already many promising signs of strategic reinvention that we will explore in this article.

The Hammer

Initially, it was thought that the health care industry would be largely unscathed by Covid-19—until it became clear within days that the loss of revenue due to primary care practices shuttering and specialists canceling elective procedures would make it among the hardest-hit parts of the economy. Hospitals and networks were forced to furlough staff, and many of those staff have still not returned to work four months later.

Carriers, on the other hand, went on collecting premiums but faced a different challenge. The giant go-to-market engines that execute annual enrollments for individual, employer, and Medicare advantage policies have traditionally relied on tens of thousands of agents sitting across kitchen and conference room tables, explaining the benefits of policies and executing tedious state-level contracts. This go-to-market engine stopped functioning overnight. Fortunately for them, the pandemic hit in a relatively slow period, giving payers months to tune their engines for the Fall. Initially, there seemed to be some question of whether the Fall enrollment would be “back to normal”—but at this point, it seems universally accepted that a new go-to-market approach will be required starting in September.

Drug companies’ cash flows were largely uninterrupted because their demand chains—pharmacies—are obviously essential businesses. But, their supply chains were severely disrupted, as countries quickly began adopting mercantilist approaches, hoarding drug precursors. Constant shortages of PPE, test reagents and supplies, and unproven “cures” to Covid-19 that have been hoarded by desperate consumers have shown what many in the FDA have known for years; that the United States’ drug supply is incredibly dependent on foreign factories, and that “me-first” mercantile policies stemming from pandemics, wars, or other unforeseen black swans could have second- and third-order health effects that outstrip the disaster itself.

At the same time, drug company research & development dollars went student-body right towards a vaccine, anti-viral, and autoimmune pipelines as the race for effective therapeutics seemingly subsumed everything. Conducting clinical trials for non-COVID drugs also became incredibly challenging, as the Doctor’s visits required for assessment, treatment, and monitoring became non-essential and fraught with risk.

The Dance

These initial “hammer” impacts on the health care industry essentially unfolded between mid-February and mid-April. By that time, most companies had grasped the nature and gravity of the existential issues that faced their businesses. Daily panic was replaced with weekly panic—as the shocks became less frequent and more manageable. This roughly correlated with the time that the stock market regained its footing, as investors, like executives, again became able to obtain and process information. Around mid-April, the health care industry began “The Dance”, which most have accepted will last for at least another nine months—and probably longer.

Hospitals

Elective procedures are how hospitals in America make money. Elective procedures have restarted in most states, but it’s increasingly clear that COVID surges will force hospitals to be much more flexible in scheduling, canceling procedures in a way that will be very frustrating for patients. Just a few days ago, Texas canceled elective procedures in hard-hit counties to deal with an upcoming wave of COVID. Actions like this will most likely continue in states that see test-positive rates climb above 10% and new cases rise due to community spread (currently, this seems to be the sunbelt states, with Texas, Florida, and Arizona getting most of the press.) However, this is still an oversimplification. In Florida, for example, 43% of new cases are hitting just three counties as of June 29th: Miami-Dade, Broward, and Palm Beach, a contiguous urban area not dissimilar to the NY-NJ-CT or MD-DC-VA megaplexes. Sumter County—the oldest demographic county in the United States and home to The Villages retirement community—is still seeing very few cases.

What to Look For:

- Hospitals will “surge” their elective procedures in periods of ebbing COVID infections, essentially building up reservoirs of cash for clear-the-deck moments.

- More flexible elective procedure scheduling will demand better use of AI to slot patients into the right slots based on upcoming disease surges, relative seriousness of the issue, and risk.

- Regional hospital networks that can move patients between hospitals will have big advantages over smaller hospitals that are frozen in one epidemiological environment. For example, hospital networks in Florida that can take advantage of low-incidence facilities will potentially have an advantage—while being careful to avoid the potential debacle of seeding the virus to low-incidence areas.

Primary Care Physicians

Most primary care networks have adapted to the drop in in-person demand (temporarily) by embracing video well visits for routine care. However, these visits are no substitute for the real thing. On a recent visit, for example, I was told that my camera’s resolution wasn’t good enough to diagnose a skin issue. More serious issues will simply be undetectable by these types of issues. This is for people who have broadband internet; much of America, still, does not. In rural areas, the cost to get 100-megabit broadband “the last mile” is simply too high.

Pediatricians are a particular area of concern due to their key role in vaccinating children, thereby maintaining the level of herd immunity required to keep other deadly diseases—like Measles, Mumps, and Rubella—at bay. Parents, afraid to expose their children or themselves to COVID, might be avoiding scheduled shots, assuming that they will receive them when this has all died down. In Florida, this has led to a 15% drop in childhood immunizations year-over-year.

What to Look For:

- To serve patients without broadband, providers will provide temporary WiFi in their clinic parking lots, so patients can do video well-visits from their cars like Hudson Headwaters and PrimeLink did in rural upstate New York.

- Annual physicals will make aggressive use of pre-visit testing, via kits sent to the home for colorectal cancer or A1C screening such as those provided by EverlyWell, or at “COVID-proof” labs to minimize contact.

- PCPs will make more use of AI-based diagnosis algorithms to track which patients need to be seen in-person, vs. putting all patients on fixed schedules.

- The days of the house call might be returning, particularly in low transmission-risk settings. Pediatricians will make use of outreach vans to reach kids who need to be vaccinated while performing other well-visit functions.

Dentists

Dentists face a particularly thorny problem. They spend all day in patients’ mouths, making the risk of transmission extremely high. A dental visit in the age of COVID is all of a sudden a very high-risk undertaking. To deal with this, Dentists have had to seriously gear up when it comes to PPE. This isn’t inexpensive—N95 masks, for example, are currently going for around $10 per mask on the open market. Add the cost of a disposable gown, gloves, and a face shield and you’re up to $20 minimum per visit in additional costs. Adding air filtration, UV disinfection, fever check stations, and other hard goods might run a small office up to $100,000 in one-time capital improvement costs.

What to Look For:

- Successful practices will adapt by changing their physical spaces. Look for larger footprints, HEPA filtering systems, and even opening windows. Patients concerned with COVID will pay a premium for these features.

- Dentists and hygienists will most likely eventually use some type of rapid-result COVID test, being tested weekly or even daily.

- Dental insurers might add a certification to their various network tiers assuring that in-network dentists have matched a certain level of protection. In exchange for this, and co-marketing the insurance company, a PPE allowance might be made (all pending the State regulators, of course.)

Payers

Payers “lucked out” early on in the pandemic as claims fell dramatically. This happened across the board for insurers—car insurers made headlines in April for refunding premium to drivers given the number of miles driven—which is very predictive of claims—fell by 70% overnight. However, now payers are realizing that they need to share some of that actuarial windfall with their providers. For primary care physicians, this means increasing payments for virtual services; for Dentists, it’s meant paying for some PPE.

Payers have more to worry about when it comes to enrolling and renewing members. As employers have shed payrolls in response to weak demand, more employees have had to move to COBRA. It remains to be seen where these employees will go—will they be re-hired in a v-shaped recovery, move to an ACA plan, or drop coverage? Unfortunately, given the cost of major medical insurance, the country will most likely see a significant drop in coverage rates for the next several quarters. Companies will come back harder than ever on rates in the upcoming enrollment season—particularly given lower claims this year.

Medicare Advantage payers are likely to dodge this bullet. Seniors are very concerned about COVID, for good reason, and will be looking for plans that provide the best COVID coverage. This will likely mean payers that position video visits, remote testing, coverage in case of hospitalization, and a proactive vaccine approach will have a leg-up during the annual enrollment period this fall. However, MA payers face a huge challenge in enrolling seniors without in-person meetings.

What to Look For:

- This could be the year when average premium increases stay nearly flat, as carriers crawl over one another for new groups to offset employee losses, and employers demand a break given lower claims. And, all of this will happen without in-person enrollment meetings, most likely providing another positive kick for benefits administration software providers, particularly those with a solid mobile experience.

- Medicare Advantage carriers will dramatically ramp up their call center and online games. Those that have built up solid internet enrollment experiences will have a big advantage this year. The combination of COVID and the ever-more-savvy 65+ demographic will make online enrollments the plurality for at least a few payers.

- Generally, look for better payer-provider relationships, as it becomes clear that the two parties are in this together. The alternative—Medicare for All—is probably more realistic now than ever before, even with Biden as the Democratic nominee. Finding ways to provide better care at a lower price has never been more imperative than it is now; in other words, if not now, then when?

Pharmaceutical Companies

People still need their prescription drugs—at least for diagnosed conditions. However, the diagnosis engine that creates cash flow for drug companies is severely busted. New diagnoses are down across the board, meaning new prescriptions to treat those conditions are also down. At the same time, without the goading of annual well-visits, drug adherence is also falling.

What to Look For:

- Drug companies will shift their detailing engine away from a “prescribe my drug” approach and towards a cooperative diagnosis approach. Like dentists relying on payers for PPE, Doctors will happily take drug company assistance in getting their practice running safely and virtually. Look for partnerships between remote diagnostic companies, wearables, drug companies, and Doctors to get diagnoses back on track.

- The process of moving supply chains back to the United States has one huge obstacle: cost. This will most likely be a political story as well as an economic one. A new administration making repatriating large parts of the U.S. drug supply chain seems likely, with both campaigns at least theoretically behind the idea—but this will be a long-time coming.

Look for Retail and Tech versions of this analysis in the coming two weeks